Darren Hosiosky

The email lands from one of the partners with "FYI" in the subject line. It's about AUSTRAC, Tranche 2, and a 1 July deadline. By the time it reaches the admin team, it's been forwarded a few times, and nobody's quite sure what it means in practice. Just that something has to happen, and soon.

AML Tranche 2 is the change that brings Australian accounting firms into the country's anti-money-laundering regime for the first time. It hasn't come out of nowhere, and it isn't a tick-box. To see what it means for your firm, it helps to know how we got here, why it's landing on accountants, and what it actually changes day-to-day.

Australia has had anti-money-laundering laws for a long time, but they only ever covered banks, casinos and money remitters. The professions that help people move money and build structures, accountants, lawyers and real estate agents, were left out. For more than a decade, the global financial-crime watchdog (the Financial Action Task Force) flagged that gap and pushed Australia to close it. Tranche 2 is that gap finally closing.

The why is straightforward once you say it plainly. If someone wants to hide where money came from, a company, a trust or a property purchase is a handy place to put it. The people who set those up sit at the exact point where suspicious money can be noticed or waved through. The reforms treat firms as part of that line of defence rather than bystanders to it, which is why accountants are now in scope.

Then this is the part that lands on the firm. From 1 July 2026, practices providing certain services have to verify who their clients really are, identify the actual people behind each entity, watch for anything that doesn't add up, and keep doing it over time. Most of that work falls to the admin and support team, on top of lodgements, signatures and follow-ups they already carry. The firms that feel it least are the ones that build a repeatable process before the deadline, not after it.

Before any of that, though, it helps to know what the words mean.

What is AML/CTF Tranche 2?

So who's actually captured? Tranche 2 brings in accountants, lawyers, conveyancers, real estate agents and others who provide what the rules call "designated services". Being in the named group doesn't automatically mean every part of your work is covered.

Not every service your firm offers is captured. The obligations attach to specific designated services (things like acting for a client on certain transactions, managing client money, or helping set up companies and trusts). So the first job is working out which of your services are actually in scope. The rules are still settling, so check AUSTRAC's current guidance for the detail rather than relying on a forwarded summary.

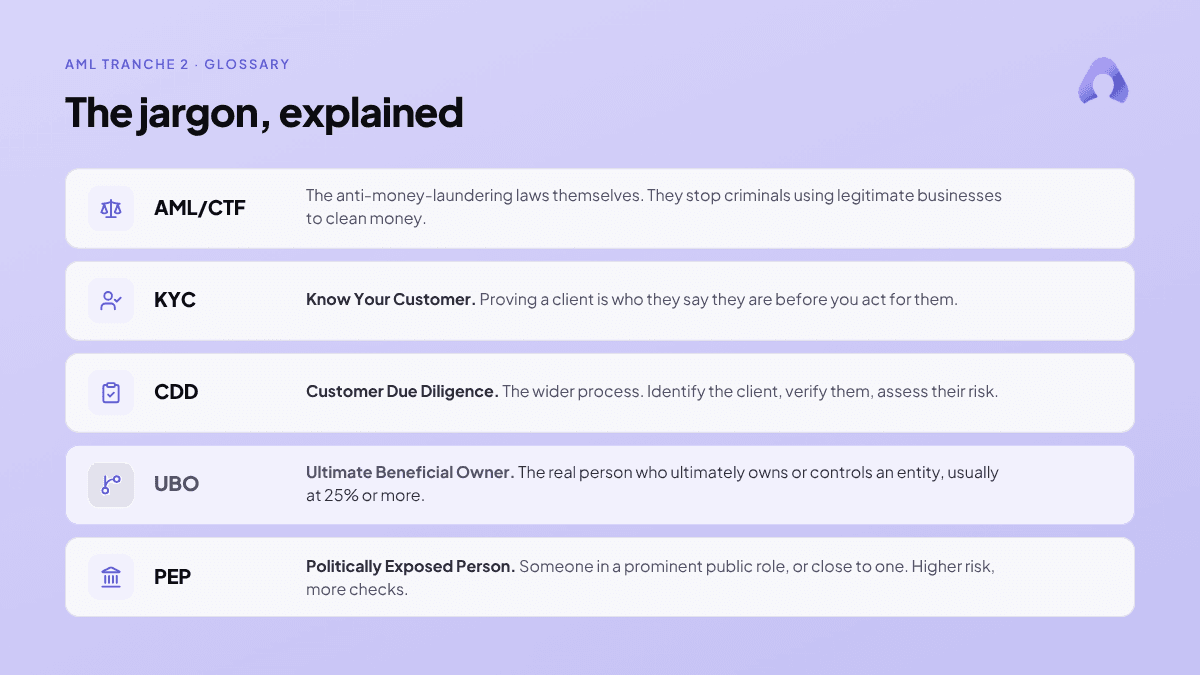

The jargon, in plain English: KYC, CDD, UBO, PEP

You'll see the same acronyms over and over. Here's what they mean.

AML/CTF (Anti-Money Laundering and Counter-Terrorism Financing): the laws themselves. The point is stopping criminals from using legitimate businesses, including accounting firms, to clean money or move funds for terrorism.

KYC (Know Your Customer): proving a client is who they say they are before you act for them.

CDD (Customer Due Diligence): the wider process around KYC. Identify the client, verify them, and assess how much risk they carry.

UBO (Ultimate Beneficial Owner): the real person who ultimately owns or controls an entity, usually at 25% or more.

PEP (Politically Exposed Person): someone in a prominent public role, or close to one. Higher risk, so more checks.

Why ultimate beneficial owners (UBOs) are the hard part

For a sole trader, KYC is simple. You're verifying one person.

It gets harder fast with your SME clients. A client might be a company owned by a family trust, with a corporate trustee, controlled by two individuals who also sit behind a second entity. To meet the obligation, you have to trace through all of that to the actual humans at the end and verify them.

Most mid-tier client books are full of exactly this: grouped entities, layered trust structures, multiple signatories. Doing that tracing by hand, client by client, is where the work piles up.

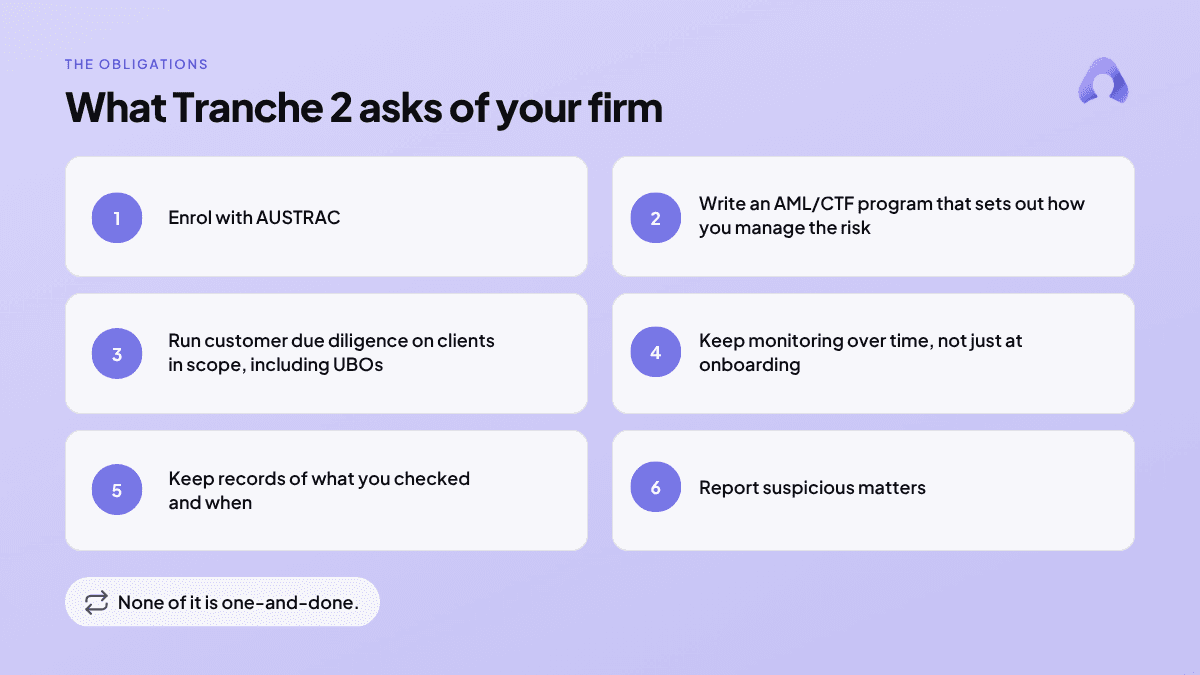

What Australian accounting firms need to do for Tranche 2

The specifics depend on your firm's risk and the services you provide, but the shape of it looks like this:

Enrol with AUSTRAC

Have a written AML/CTF program that sets out how you manage the risk

Run customer due diligence on clients in scope, including identifying and verifying UBOs

Keep monitoring on an ongoing basis, not just at onboarding

Keep records of what you checked and when

Report suspicious matters

None of it is one-and-done. The monitoring piece means a client you verified last year can't just sit untouched.

The real challenge: AML compliance at volume

Understanding the obligation is the easy part. Meeting it across a full client book during BAS or ITR season is the hard part.

The old way of verifying identity (posting forms, copying licences, chasing clients for documents, logging it all somewhere) was slow when it was occasional. Done at scale, on top of everything else the admin team already carries through a busy period, it becomes its own backlog.

How in-workflow KYC screening helps

This is the problem Admiin is built to take off the admin team's plate.

Admiin runs KYC and AML screening inside the same lodgement workflow you already use to prepare and send documents. After you send an engagement letter or a tax doc, verification is one click: document checks via DVS, PEP and sanctions screening, KYB and UBO identification across the structure.

When a deadline is bearing down, you can bulk verify up to 1,000 clients at once instead of one at a time. The screening is AUSTRAC compliant, and a single dashboard shows status, what's cleared, what's failed, and why. No separate tool, no second login, no rekeying client details you've already entered.

The core product is free. No subscription trap, no forced payments.

A sensible place to start

Tranche 2 isn't going away, and the monitoring obligation means it's not a job you finish. So the firms that handle it best are the ones who make verification part of the normal workflow rather than a separate scramble.

If Tranche 2 is on your list this quarter, it's worth seeing what verifying a client looks like when it's one click instead of a process. Sign up free to try it, or book a demo and we'll walk through it on your own client structures.

Frequently asked questions

When does AML Tranche 2 start in Australia?

Obligations for the newly captured group, including accounting firms, are set to apply from 1 July 2026, with enrolment ahead of that. Confirm the current dates and enrolment window on AUSTRAC's website, as timing and detail can change.

Does Tranche 2 apply to all accountants?

No. It applies when a firm provides specific "designated services" under the AML/CTF rules. Some of what your firm does may be in scope and some may not, so the first step is mapping your services against the rules.

What is an ultimate beneficial owner (UBO)?

A UBO is the real person who ultimately owns or controls a client entity, usually at 25% or more ownership or control. For clients structured through companies and trusts, you have to trace through the layers to the individuals behind them.

What's the difference between KYC and CDD?

KYC (Know Your Customer) is the part where you confirm a client's identity. CDD (Customer Due Diligence) is the broader process that includes KYC, plus assessing the client's risk and keeping that assessment current over time.

Do I have to re-verify existing clients?

The regime includes ongoing customer due diligence, so verification isn't a one-time step at onboarding. How and when you review existing clients depends on their risk and your AML/CTF program. Check AUSTRAC's guidance for what applies to your firm.

Is there software that handles AML checks for accounting firms?

Yes. Admiin runs AUSTRAC-compliant KYC and AML screening inside the lodgement workflow, including DVS, PEP, sanctions, KYB and UBO checks, with bulk verification of up to 1,000 clients. The core product is free.

This is general information, not legal or compliance advice. Your obligations depend on the services your firm provides. Check AUSTRAC's current guidance, or your own adviser, for what applies to you.