Darren Hosiosky

The Silver Tsunami in Australian Accounting: Why Firm Succession Is About to Reset

There is a conversation happening between Australian accounting partners and their advisers right now that doesn't make the agenda at any CAANZ panel. It rarely surfaces at industry roundtables. It almost never appears in trade press.

The conversation is about who, exactly, the firm is going to be sold to.

For most of the last forty years, the answer to that question was either obvious or available. A senior associate would step up and buy in. A neighbouring firm would merge. Worst case, the practice would be wound down with the client book sold to a friendly competitor. The economics worked. The buyers existed. The retiring partner walked out with a number that justified the years.

That answer is breaking. The reasons are demographic, economic, and structural — and they are reshaping the Australian accounting succession market on a timeline most partner groups have not yet absorbed.

The arithmetic the next generation has already done

The supply-side data is well-rehearsed. Across CAANZ, CPA Australia, and the recruitment market, the trend has been visible for half a decade. A substantial majority of Australian accounting firm equity partners are over 50. A meaningful tail is over 60. The retirement curve in front of the profession isn't a gentle slope. It's a wave.

The demand-side data is the part that gets less airtime, partly because it is uncomfortable for the cohort still in the partner room.

Fifteen years ago, the senior associate calculating whether to buy into partnership ran a relatively favourable equation. Buy-in was generally in the $250k to $400k range, financed across five to seven years out of partner drawings. Hours were demanding but predictable. Equity compounded. A retiring partner exited with a number that materially affected their financial life.

The same calculation in 2026 produces a different result. Buy-ins have climbed to $400k–$800k at metro firms, with some larger mid-tier shops crossing $1m. Partner drawings have not kept pace, because rising labour costs and compressed pricing have eaten margin. The compounding period before equity becomes meaningful is longer. The exit, when it arrives, is softer than the prior generation experienced.

Meanwhile, the alternatives have improved materially. A corporate finance role at a listed Australian company offers competitive base salary, RSUs that have actually appreciated, and a 45-hour working week. A finance lead at a Series B fintech offers similar with options that could be worth nothing or could be a house. Treasury seats at the major banks pay strongly with explicit work-life boundaries. The professional bodies have, almost without intending to, made these alternatives more accessible by maintaining the rigour of the qualification while doing nothing to fix the partner-track economics.

The senior associates and managers walking away from the partnership conversation are not lazy. They are not disloyal. They are simply better at pricing options than the partner group above them tends to acknowledge.

Three succession doors — and why two of them are jamming

Ask any 55-plus principal what their succession plan looks like, and the answer almost always falls into one of three categories: an internal buyout, a merger with a neighbouring firm, or a sale to private capital. Each of these doors operates differently in 2026 than it did in 2019.

Door one: the internal buyout

The internal buyout is the option most retiring partners still believe they are walking through. The structure is elegant on a whiteboard. Identify two or three high-performing senior managers. Structure a multi-year buy-in financed out of drawings. Progressively dilute the retiring partners. Glide path to retirement. Everyone wins.

The structure depends entirely on the existence of two or three high-performing senior managers who actually want to buy in. As partner groups across Australia are increasingly discovering, those people are scarcer than the model assumes. When firms run the maths honestly, the internal buyout often only works if the existing partners accept a discount on their equity to make the entry economics attractive to the new partners.

A pay cut at retirement, dressed up as a succession plan.

Door two: the merger with the firm down the road

The neighbouring-firm merger has been the Australian default since the 1980s, and it still works in some configurations. Two suburban firms with complementary client books, overlapping admin functions, and reasonable cultural fit can produce a real synergy story.

The configuration it doesn't work in is the one most firms are now in: two metro practices, both with ageing partner groups, both facing the same pipeline problem. Merging produces a larger firm with the same demographic and operational challenges. There is generally a moment, somewhere between sixty and ninety days post-integration, when both leadership groups realise the combined succession problem isn't 1+1. It's closer to 1×1.

Mergers between two firms with identical problems do not solve the problem. They concentrate it.

Door three: private equity (late, but coming)

The third door is the one most retiring partners now talk about hopefully, often without naming it directly.

In the United States, private equity has fundamentally transformed mid-tier accounting. EisnerAmper, Aprio, Citrin Cooperman, and Baker Tilly US have all completed meaningful PE-backed transactions in the last five years. In the UK, Waterland is rolling Cooper Parry. HG owns Azets. IK Partners holds Evelyn. The investment thesis is straightforward: acquire a regional firm at six times EBITDA, bolt on three more at five, automate the back office, expand advisory revenue, exit at ten.

In Australia, the playbook has not yet fully arrived. Kelly+Partners is the listed exception, acquiring at a measured pace rather than aggressively. Findex has its own private-capital story. Pitcher Partners has stayed federated and partnership-owned. Private capital has been evaluating the Australian mid-tier for two years.

The dedicated Australian roll-up vehicle has not yet emerged at scale. The best available analysis suggests it will, probably within the next twenty-four months. The retiring partners betting on its arrival have been making that bet since 2023.

The variable that quietly changes the multiple

The doors-and-keys framing of succession misses the most consequential variable in modern accounting M&A. Every conversation about firm sale assumes the firm being sold tomorrow looks operationally like the firm being run today.

It doesn't, and the gap between those two firms is where most of the value moves.

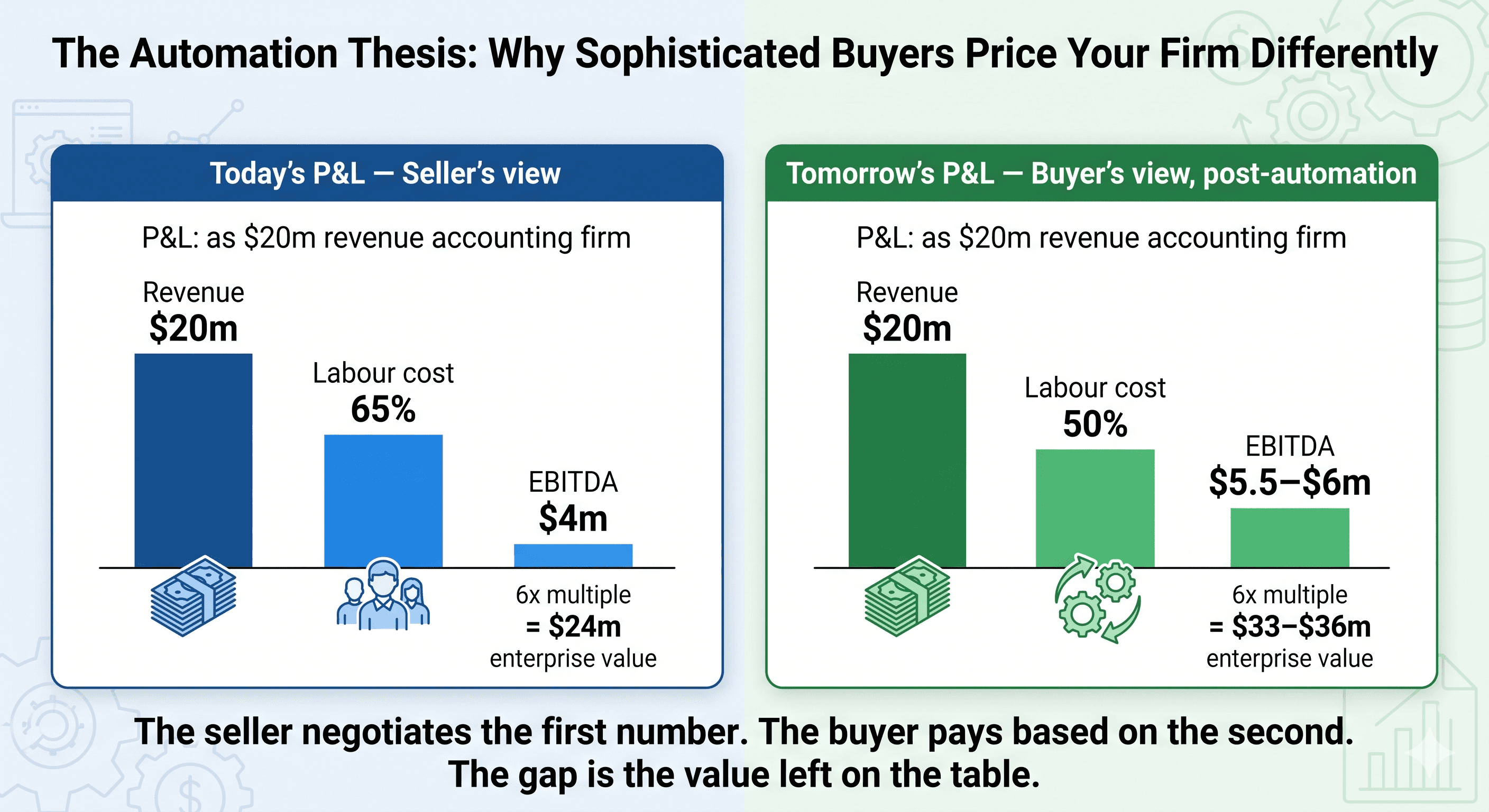

Take a representative metro firm with $20m in revenue and $4m in EBITDA. Labour costs typically run between 60 and 70 per cent of the cost base. Within that labour cost, a meaningful proportion — call it 25 to 35 per cent — is genuinely automatable. Not in the marketing sense. In the mechanical, code-replacing-keystrokes sense. Cover letter generation. Tax binding assembly. ATO portal navigation. ASIC annual review chasing. KYC verification under the AUSTRAC Tranche 2 regime. E-signature follow-up loops. Workpaper rollforward. Client onboarding and document collection.

If a buyer can automate 30 per cent of the cost base post-acquisition, EBITDA on the same revenue moves from $4m to approximately $5.5–$6m. At a 6x multiple, enterprise value moves from $24m to $33–$36m. Before any growth thesis on advisory expansion is even introduced.

This is the quiet asymmetry at the centre of the Australian succession market. The retiring partner is selling a firm priced on today's labour-heavy P&L. The sophisticated buyer — and this is what private-equity sophistication actually means, more than the capital itself — is buying the same firm priced on tomorrow's automated P&L.

The seller sees a 5x multiple and feels reasonable. The buyer is modelling a 3x multiple on the post-automation EBITDA they intend to engineer in the first two years, and feels generous.

Who wins this negotiation? The buyer with the playbook. Consistently.

The retiring partner who runs an unsophisticated process — speaks to one PE intermediary, talks to the firm down the road, accepts the first reasonable number — leaves a third of the eventual value on the table. The retiring partner who runs a sophisticated process, with multiple bidders all working from the same automation thesis, captures most of it.

Most retiring partners will run an unsophisticated process.

Three Australias, three different succession problems

The Australian accounting M&A market is not one market. It is three, and the arithmetic above plays out very differently in each.

The mid-tier

Your BDOs, Findexes, Grant Thorntons, William Bucks, HLBs. These firms generally have functioning internal pipelines, but the partner buy-in is expensive enough that the recruitment problems compound at the senior manager level. Mid-tier firms will be acquirers in the coming roll-up cycle. The well-run ones know it. Their succession challenge is at the partner-equity layer, not the firm-survival layer.

The metro independents

Five to fifteen partners, $5m to $30m in revenue, advisory-leaning, usually in a CBD tower. This cohort is the most exposed to the coming reset and the most attractive to private capital. Too large to be absorbed by a neighbouring firm. Too small for an IPO. Perfectly sized to be the cornerstone of a roll-up platform or the third or fourth bolt-on.

If your firm sits in this category, the next eighteen months will determine whether you sell into a competitive process or sell because you have to. Those two transactions produce very different multiples.

The suburban two-and-three-partner firms

The quietest tragedy in the market. Compliance-heavy, ATO-portal-centric, often single-principal, with client books that are substantially automatable inside the next 36 months. Five years ago these firms traded to a slightly larger neighbour at one to one-and-a-half times revenue. The neighbour now has the same problem, and the price has softened. In some suburbs the only buyer is the local bookkeeper consolidating upward, paying in earn-out rather than cash.

For this cohort, succession is increasingly less about finding the best buyer and more about finding any buyer who is willing to acquire a labour-heavy compliance practice in a market where the buyer's own demographics are deteriorating.

Selling into the wave or after it

For any partner group running a firm sized $5m–$30m in revenue, the strategic question for 2026 isn't whether to sell. It's whether to sell into the wave or after it.

Selling into the wave means accepting that the 2026–2028 buyer will be more sophisticated than the 2019 buyer would have been. They arrive with an automation thesis, a roll-up playbook, and the institutional patience to walk away from a transaction that doesn't price in the post-automation earnings.

The seller who matches that sophistication arrives at the negotiation with:

Clean, structured financial data

Documented operational processes

A client book segmented by margin contribution and automation potential

A credible internal staffing thesis for the post-acquisition firm

At least three credible bidders running on the same timeline

An adviser with prior roll-up sale experience, not the local tax partner's golfing acquaintance

Selling after the wave means waiting until the PE platforms have completed their first ten Australian acquisitions, multiples have compressed, and the market has normalised around the automated mid-tier P&L. By that point, a labour-heavy practice without an automation story of its own is a late-cycle seller in a buyer's market. There will still be an offer. It will not be the number the partner group expected.

The eighteen-month window matters because the buyer playbook is arriving in Australia regardless of what any individual firm does. The strategic decision is whether to arrive with it, or after it (we expand the broader thesis in the 36-month reset facing Australian accounting firms).

How firms get sale-ready under the automation thesis

A partner group eighteen months out from a potential transaction can usefully run through a structured readiness checklist with their CFO and external adviser.

Map the engagement-to-lodgement workflow. Where does an admin team member touch each job? How long does each touch take? Multiply by fully-loaded labour cost. The resulting number is generally larger than the partner group has previously articulated.

Audit the tech stack. How many software products does the firm pay for? How many are genuinely used? Tool sprawl is the single most common operational finding that depresses due diligence outcomes.

Document the processes. Buyers consistently value documented operations over institutional-knowledge operations at a measurable multiple premium. If the firm runs on the institutional memory of two partners and a long-tenured practice manager, the buyer will price in transition risk.

Embed AUSTRAC Tranche 2 compliance into the workflow before 1 July 2026. Buyers conducting due diligence in 2027 will treat AML/CTF readiness as binary. Either it is operationally clean, or it is a project the buyer has to fund.

Segment the client book. Margin per client, automation potential per client, retention risk per client. Make the segmentation explicit and visible. Buyers reward sellers who have already done the analysis.

Develop an internal staffing thesis. Which roles persist, which restructure, which redefine post-automation. Build the answer before the buyer constructs their own version.

Run a competitive process. Single-bidder transactions are the most common cause of value left on the table at sale.

How Admiin fits into a sale-ready firm

Admiin is the AI workflow automation layer that enables an Australian accounting firm to present to a buyer as operationally clean and already automated, rather than as a renovation project the buyer has to underwrite.

The buyer's automation thesis in 2026 depends on five workflow surfaces. Admiin operates across all of them:

AI-generated tax cover letters and binding preparation

AUSTRAC Tranche 2-aligned KYC, customer due diligence, and beneficial ownership capture

E-signature workflows built for tax-firm document types

Embedded payments including Apple Pay, Google Pay, and credit card for ATO liabilities

Practice workflow orchestration and automated client follow-ups

The operational difference between a firm running on Admiin and a firm running on a fragmented stack of FuseSign or Annature for signing, Practice Ignition for engagement, XPM or Karbon for practice management, a separate KYC vendor, and seven Outlook folders, is the difference between a clean automation thesis the buyer pays a premium for and a renovation project the buyer discounts.

Eighteen months is generally enough time to build the first version. It is not enough time to build it from a standing start in the final quarter before sale.

Frequently Asked Questions

What is the average sale multiple for an Australian accounting firm in 2026? Multiples vary considerably by tier, region, client mix, and operational quality. Suburban two-and-three-partner firms commonly trade at 0.8 to 1.2 times revenue. Metro independent firms typically trade in the 4–6x EBITDA range. Mid-tier and PE-backed transactions can reach 7–9x EBITDA for clean assets with strong advisory exposure. The variable that increasingly moves the multiple is operational automation — sophisticated buyers price the post-automation P&L rather than the current one.

Is private equity active in Australian accounting? Selectively, and arriving in size shortly. Kelly+Partners is the listed exception. Findex has its own private-capital story. International PE-backed accounting platforms have been evaluating Australian entry for approximately two years. The dedicated Australian roll-up vehicle has not yet emerged at scale, but credible analysis expects meaningful PE-driven mid-tier activity within the next twenty-four months.

What's the difference between selling to a competitor and selling to a private-equity-backed buyer? A competitor typically values your firm on current EBITDA, current staffing, and synergy with their existing client book. A PE-backed buyer values your firm on the post-acquisition EBITDA they can engineer through automation, advisory expansion, and operational consolidation. PE buyers are generally more sophisticated and harder to negotiate against, but they often pay more if the firm is presented properly with a credible operational story.

How long does succession planning take for an Australian accounting firm? Realistically, three to five years from decision to clean exit when the path is internal buyout. Eighteen to twenty-four months when running a competitive external sale process. Six to nine months when the firm is in distress and accepting a discounted single-bidder offer. Most firms underestimate the timeline and start the process too late.

How does AUSTRAC Tranche 2 affect firm valuation? Significantly. From 1 July 2026, AML/CTF compliance is binary in due diligence. Buyers will price a firm with clean, embedded AUSTRAC workflows differently than a firm with a paper policy and limited operational readiness. Tranche 2 readiness is a value-protection issue, not just a compliance issue.

Can a firm be made sale-ready in eighteen months? Yes, but only if the partner group commits to genuine operational change rather than cosmetic readiness. Eighteen months is sufficient to document processes, embed AML/KYC workflows, consolidate the tech stack, automate the admin substrate, and segment the client book. It is not sufficient to fix a deeply fragmented firm with no documented operations from a complete standing start.

Should I sell now or wait for higher multiples? The honest answer is that multiples for clean, automated firms are likely to hold or rise as private capital arrives. Multiples for labour-heavy, undocumented firms are likely to soften as the market normalises around the automation thesis. The strategic question isn't really "now versus later" — it's "ready versus unready when the timing is forced."

Don't sell into someone else's automation thesis

Eighteen months from a potential sale, the difference between a firm running on Admiin and a firm running on a fragmented stack is the difference between a clean exit multiple and a renovation discount. The buyer is going to model the automated P&L either way. The strategic question is whether they pay you for it or build it themselves after settlement.

See what a sale-ready workflow looks like →

SUPPLEMENTARY FIELDS (Article 3)

Internal Linking Suggestions:

AI-generated tax cover letters and binding preparation→ /ai-tax-cover-lettersAUSTRAC Tranche 2-aligned KYC, customer due diligence→ /aml-ctf-kyc-complianceE-signature workflows built for tax-firm document types→ /e-signature-for-accountantsEmbedded payments→ /paymentsPractice workflow orchestration→ /practice-workflow-automationAutomated client follow-ups→ /client-reminders-automationFuture cluster: The 36-Month Reset → /blog/australian-accounting-firms-2029-reset

Future cluster: Will AI Replace Accountants in Australia → /blog/will-ai-replace-accountants-australia

Future cluster: Preparing your firm for AUSTRAC Tranche 2 → /blog/austrac-tranche-2-readiness-australia

Future cluster: How to value an Australian accounting firm → /blog/how-to-value-australian-accounting-firm

Future cluster: Admiin vs FuseSign → /blog/admiin-vs-fusesign

Future cluster: Admiin vs FuseSign → /blog/admiin-vs-fusesign