Darren Hosiosky

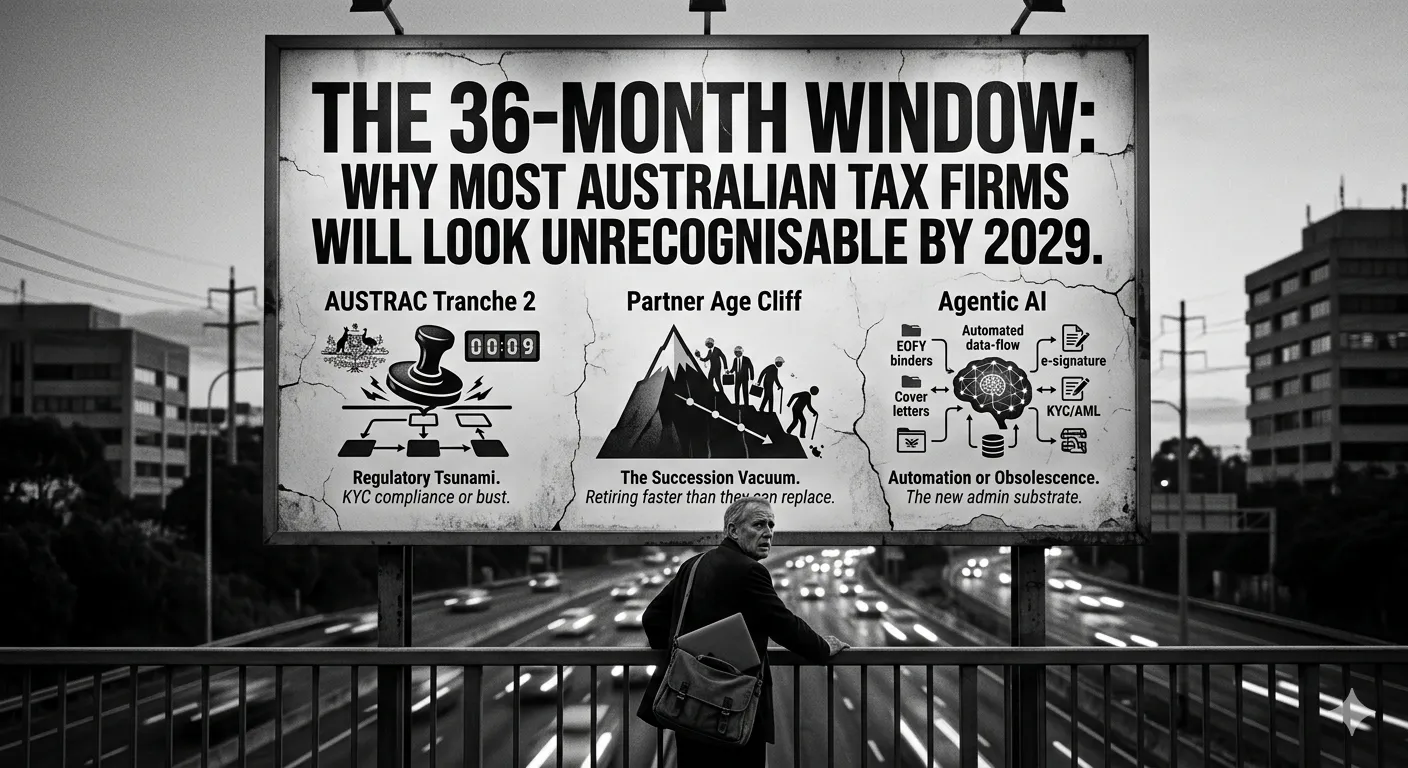

The 36-Month Reset: How Australian Accounting Firms Will Be Restructured Before 2029

Walk into the average mid-sized accounting firm in Australia on a Tuesday afternoon and the operational picture looks much like it did fifteen years ago. Practice managers triaging emails. Admin staff manually re-uploading client identity documents because the previous file format wouldn't open. A senior associate reformatting a tax cover letter for the third time because the draft template lives on someone's desktop. Partners on calls about lodgement deadlines.

Profitable firm. Loyal clients. Stable revenue. No obvious reason to think 2029 will look different from 2024.

That reasoning is wrong, and the lead time available to do something about it is shorter than most partner groups have priced in.

Why "incremental change" is the wrong mental model

The temptation, when reading any "the industry is changing" piece, is to mentally file it under something to look at next quarter. That instinct is usually correct. Most predictions don't materialise on the timeline the writer claims, and most firms can absorb gradual change inside existing operations.

This isn't that.

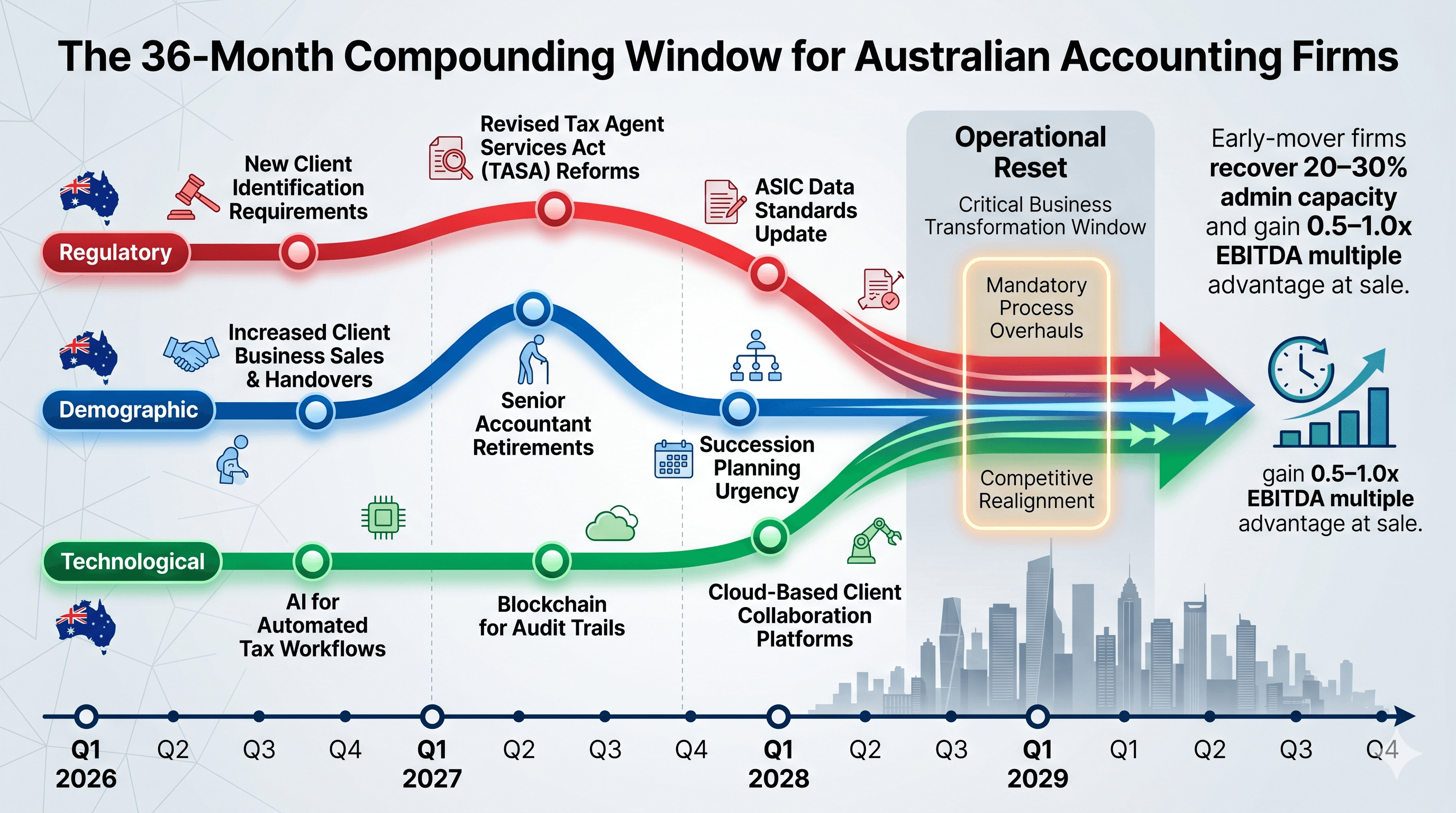

The next three years are unusual because three independent structural forces — regulatory, demographic, and technological — are arriving at the same Australian accounting firm simultaneously. Each one in isolation would be a manageable project. Stacked on top of each other, they produce a different kind of problem: one where the response cost grows faster than the partner group's available bandwidth, and where deferring the response doesn't shrink the problem, it compounds it.

Understanding why requires looking at each force separately first.

The three forces converging on Australian accounting firms right now

Regulatory pressure: AUSTRAC Tranche 2 lands on 1 July 2026

Tranche 2 of Australia's AML/CTF reforms formally extends the regime to tax agents, accountants, conveyancers, and other designated professional service providers from 1 July 2026. For the accounting profession specifically, this is the largest regulatory change since the introduction of GST.

The obligations are substantive:

Customer due diligence (CDD) at the point of engagement

Ongoing CDD applied to existing client books

Beneficial ownership identification for entity clients (trusts, companies, partnerships, SMSFs)

A written AML/CTF compliance program

A designated compliance officer with explicit responsibilities

Suspicious matter reporting to AUSTRAC

Record retention obligations stretching seven years

What most firms underestimate is that Tranche 2 is not really a compliance project. It's a workflow project disguised as a compliance project. Done properly, the obligations are absorbed into the engagement-to-lodgement workflow and run in the background. Done as a separate parallel track — with a policy document, a quarterly checkbox, and an outsourced AUSTRAC consultant — the costs accumulate every year and the audit risk never really resolves.

Firms that build AUSTRAC compliance into how new clients are onboarded will spend less per year, in perpetuity, than firms that bolt it on. That's a workflow decision that has to be made before July 2026, not after.

Demographic pressure: the partner exit wave is real and accelerating

The partner-age data has been visible for years across CAANZ surveys, CPA Australia benchmarks, and the recruitment market. The simplified version: the equity-partner cohort in most Australian mid-tier and suburban firms skews heavily 50-plus, with a meaningful tail past 60 (we go deeper on the resulting M&A dynamics in the Australian accounting firm succession reset).

The supply problem is well-rehearsed. The demand problem is less so.

The senior managers who would historically have stepped up into partnership have been quietly opting out of the equity path for the better part of a decade. Buy-ins have escalated from the $250k–$400k range to anywhere between $500k and $1.2m at metro firms. Drawings haven't kept pace, because rising labour costs are compressing partner margins. The compounding period before equity becomes meaningfully valuable is longer than the prior generation faced.

Meanwhile, industry roles — corporate finance positions at listed companies, finance leads at growth-stage technology firms, treasury seats at the major banks — pay competitively for roughly half the hours and offer liquid equity rather than illiquid partnership stakes.

The result is a thinning of the natural succession pipeline. Firms that assumed they had a five-year runway to identify and develop equity successors are increasingly discovering that runway is closer to three. Firms that assumed acquirers would queue up are discovering the queue is shorter and the buyers are more sophisticated.

Technological pressure: AI that finally works on tax-firm workflows

The "AI for accountants" pitch has been around long enough to have developed a credibility problem. For most of the last five years, the demos have outpaced what the tools could reliably do in production. Cover letters that read well but used outdated figures. Document classifiers that misfiled trust deeds as company constitutions. OCR that lost decimal places.

In the last twelve to eighteen months that gap has closed materially, and it has closed in the unglamorous parts of the workflow first — which turns out to be where the largest cost base sits.

Tax cover letter generation. Tax binding assembly and pagination. Client document collection with automated chasing. E-signature workflows tailored to engagement letters, returns, and authorities. KYC capture under the AUSTRAC framework. OCR with structured data extraction. Triage of inbound client communication. Practice management entry generation from completed jobs.

None of this is taxpayer-facing advice. None of it requires the model to be "competent" in a regulatory sense. All of it is the load-bearing admin that has historically been absorbed by salaried humans pushing documents through fragmented tools.

The technology, in 2026, finally does this work properly. Reliably. With audit trails. At a fraction of the cost of the human labour it replaces.

Why these three forces compound (and why working harder won't fix it)

Each of these forces, in isolation, can be absorbed by a competent partner group running normal operations.

Tranche 2 on its own is a workstream. The succession problem on its own is a five-year plan. AI on its own is a procurement exercise.

The reason 2026 to 2029 is the structurally important window is that the three forces interact in a way that creates non-linear cost and benefit dynamics.

Consider the firm that moves early. By embedding AML/CTF compliance into the engagement workflow before 1 July 2026, it walks into Tranche 2 go-live with audit trails captured automatically rather than maintained manually. When an aggregator or private-equity-backed acquirer arrives in late 2027 or 2028 — and they will, because the playbook has already played out in the UK and US — the firm presents as an operationally clean, documented asset rather than a paper-and-spreadsheets practice. That presentation difference is worth somewhere between half and one full multiple turn on EBITDA in the eventual sale price. In the meantime, the same automation that captures KYC also frees up 20 to 30 per cent of admin capacity, which the firm can either redeploy into client growth or pocket as margin.

Now consider the firm that defers. It approaches the AUSTRAC deadline in May 2026 as a Word-document exercise. It postpones the AI decision until "things settle down." It assumes succession will sort itself out. By 2028 it is simultaneously absorbing AML/CTF retrofit costs, losing senior staff to better-organised competitors, and meeting acquirers from a position of operational weakness rather than strength.

There is no version of this scenario where the deferring firm catches up by working harder. The early-mover advantage isn't about intelligence or effort. It's about the compounding period — the time between when operational discipline is built and when it shows up in the firm's metrics — which is approximately eighteen months. That period has to run before the firm sees the benefit. It cannot be shortened.

A practical readiness audit for the partner reading this

If you run an Australian accounting firm of any size and you've read this far, the useful next step isn't to commission a strategy paper. It's to honestly answer six questions about your current operations.

Engagement and onboarding. Can a new client move from initial contact to signed engagement letter, with AUSTRAC-grade identity verification captured, in under 48 hours, without an admin team member chasing documents through email?

AML/CTF readiness. As of today, is your firm's Tranche 2 program documented in writing, with a named compliance officer, a tested CDD workflow, and an audit trail you would be comfortable showing AUSTRAC in 2027?

Tax document workflow. When a return is finalised, how many human hours sit between "return ready" and "client signed, paid, lodged"? In well-run firms this is well under an hour. In typical firms it's three to five.

E-signature cycle time. What is your median time from engagement letter sent to engagement letter signed? Best-in-class firms are under 24 hours. Most are over three days.

Payment friction. How do clients pay you for tax preparation work? How do they pay the ATO? If either answer involves BSB numbers in an email, you are running 2012 plumbing in a 2026 firm.

Sale-readiness. If a credible acquirer walked through the door tomorrow, how long would due diligence take? What proportion of your processes are documented versus held in the heads of two or three people?

A firm answering "yes, confidently" to fewer than four of these is not necessarily behind — but it is sitting somewhere in the middle of the window where action this year still produces structural advantage. A firm answering yes to fewer than two is closer to the back of the window than it thinks.

Where Admiin sits in this picture

Admiin is the workflow automation platform built specifically for the operational layer that sits between an Australian accounting firm's partner group and its clients. It is the layer where Tranche 2 obligations, succession readiness, and practical AI actually meet.

The product covers the surfaces that consume the most admin capacity in a typical tax firm:

AI-generated tax cover letters drafted from finalised returns

Automated tax binding preparation and pagination

AUSTRAC Tranche 2-aligned KYC and AML/CTF workflows

E-signature for engagement letters, returns, and authorities

Embedded payments including Apple Pay, Google Pay, and credit card for ATO liabilities

Automated client reminders and follow-up sequences

OCR and structured document extraction

Practice workflow orchestration across the engagement-to-lodgement cycle

The strategic intent isn't to add another tool. It's to replace the fragmented stack — typically some combination of FuseSign or Annature for signing, Practice Ignition for engagement, XPM or Karbon for practice management, a separate KYC vendor, and seven Outlook folders — with one workflow layer that captures the audit trail once and pushes it through every downstream step.

The firms making this shift in 2026 are not doing so because automation is interesting. They are doing so because the operational discipline built in 2026 is what determines whether they sell, scale, or shrink in 2029.

Frequently Asked Questions

When does AUSTRAC Tranche 2 take effect for Australian accounting firms? Tranche 2 AML/CTF obligations extend to tax agents, accountants, and other designated professional services from 1 July 2026. From that point, in-scope firms must perform customer due diligence at engagement, maintain ongoing CDD on existing clients, identify beneficial ownership for entity clients, hold a written AML/CTF program, designate a compliance officer, and report suspicious matters to AUSTRAC.

What's the difference between Tranche 1 and Tranche 2 of Australian AML/CTF reform? Tranche 1 captured banks, financial services providers, and gambling operators. Tranche 2 extends the regime to designated non-financial businesses and professions — most notably accountants, tax agents, lawyers, conveyancers, and real estate agents. For the accounting profession, Tranche 2 represents the first time AML/CTF compliance has been a mandatory operational requirement rather than a voluntary best practice.

Will AI replace accountants in Australia by 2029? No. The regulatory architecture — the Tax Agent Services Act 2009, the Tax Practitioners Board's Code of Professional Conduct, ATO compliance requirements, and PI insurance frameworks — keeps the registered tax agent in a structurally human role. What AI is replacing is the admin substrate around the registered work: cover letters, binding preparation, KYC capture, e-signature chasing, document collection, and client follow-ups. In most firms this layer represents 30 to 40 per cent of weekly capacity (full analysis: will AI replace accountants in Australia?).

How does the partner exit wave affect smaller accounting firms? The smaller and more compliance-heavy a firm, the more exposed it is. Suburban two-and-three-partner firms historically sold to slightly larger neighbours at one to one-and-a-half times revenue. Those neighbours now have the same demographic problem, and acquirers are increasingly looking for operationally-clean, automatable practices rather than additional client books. Firms in this segment that haven't documented and automated their operations risk selling at progressively softer multiples.

What does an automation-ready accounting firm actually look like operationally? Engagement letters are signed within 24 hours. KYC is captured in the same workflow as the engagement. Cover letters and bindings are drafted automatically and reviewed rather than typed. Client follow-ups run themselves. Payments flow through embedded checkout rather than email. The admin team handles exceptions and client experience rather than data entry. The audit trail is captured once and inherited by every downstream system.

How long does it take to make these operational changes? The first eighteen months of disciplined operational change deliver most of the visible benefit. Engagement workflow redesign typically takes two to three months. AML/CTF embedment takes three to four. Document and binding automation typically goes live within the first quarter. The compounding effect — where the workflow advantage shows up in margin, client capacity, and saleability — needs the full eighteen months to fully crystallise.

Ready to start the eighteen-month clock?

The compounding window is open now, not in 2027. See what an engagement-to-lodgement workflow looks like when AUSTRAC compliance, AI document assembly, e-signatures, and payments run on one layer. Book a 20-minute walkthrough — no pitch, just the workflow.

Internal Linking Suggestions:

AI-generated tax cover letters→ /ai-tax-cover-lettersAutomated tax binding preparation→ /ai-tax-bindingAUSTRAC Tranche 2-aligned KYC and AML/CTF workflows→ /aml-ctf-kyc-complianceE-signature for engagement letters, returns, and authorities→ /e-signature-for-accountantsEmbedded payments→ /paymentsAutomated client reminders→ /client-reminders-automationOCR and structured document extraction→ /ocr-document-extractionPractice workflow orchestration→ /practice-workflow-automationFuture cluster: Admiin vs FuseSign → /blog/admiin-vs-fusesign

Future cluster: Preparing your firm for AUSTRAC Tranche 2 → /blog/austrac-tranche-2-readiness-australia

Future cluster: Will AI replace accountants in Australia → /blog/will-ai-replace-accountants-australia

Future cluster: Australian accounting firm succession planning → /blog/australian-accounting-firm-succession